Observations from a recent financing round

Observations from a recent financing round

Trends discerned from a recent financing round amidst plummeting public market multiples and renewed attention on private market valuations.

Stepping out of the operating box for a moment, I thought it was worth sharing some observations from speaking to a large cohort of investors during our recent financing raise (Colligo raised a SAFE in February).

Given the acute attention on valuations and private vs. public market dynamics, I believe this recent near real time feedback provides some insight into what’s happening in our segment of the market (pre-Series A/growth equity, nearing breakeven profitability but investing for growth @Colligo).

My unique perspective on this comes from having recently spoken to ~40 different investors (mix of VCs, angels) and aggregating the views to develop my own barometer qualitative barometer. Whether that’s a truly statistically significant sample or not, the jury is out, but it seemed like a good number to discern a few trends and observations:

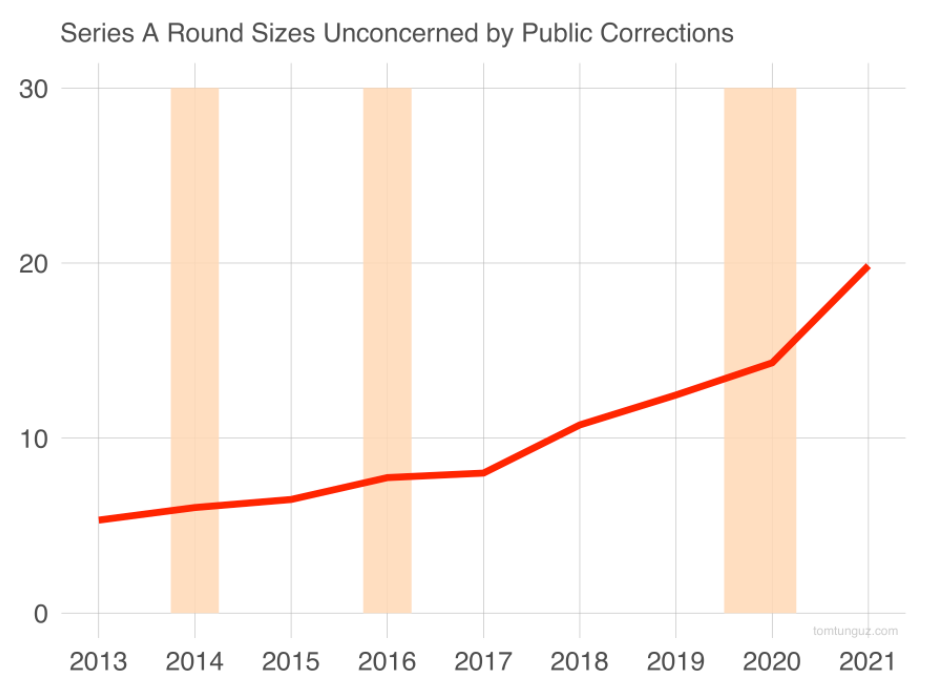

No indication of multiple compression in the early stages – appears contained to later/pre-IPO rounds, with no pushback on our proposed valuation ideology (as predicted by Tom Tunguz in mid-January). Perhaps compression flows through to earlier stages in the next few weeks…

Does appear to me that more focus is being put on “quality” (cashflow, runway, unit economics like ARPU expansion, retention). There seems to be a renewed emphasis being placed on having the ability to show a path to profitability

With our deck anyway, most time was spent on a) the market, b) the team, and c) the overview slides of our pitch deck (in order)…. thanks for the insights, DocSend

Notably, runway came up in almost every conversation, but this isn’t a significant change… maybe more weight is just being assigned to it now

There was general discussion of later stage funding is slowing down, despite the continued massive funding announcements and headlines. Many of these took place a few weeks (or even months) prior to the latest factor rotation and are just being announced now

I’ve even heard of term sheets being re-negotiated at lower multiples after they were initially agreed upon in the worst of stories

We’ve seen companies who over-hired on a pandemic pull forward now have to revert to larger layoffs (no fun)

On whole, it appears there is still a lot of capital and liquidity out there and ready to be put to work, however, I think it will be more selective and the flight to quality will persist (likely weighing more towards enterprise SaaS with proven PMF).

Further, as a wise friend of mine pointed out recently, with the focus on quality, companies may be staying private for longer in order to mature… does this bring more capital to private markets? or does it force later stage investors to move to earlier segments of the market? Rising rates, rampant inflation and geopolitical instability should further accentuate this for some time… perhaps we are entering the era of durable and sustained growth > growth at all costs.